In finding out what the Future of Corporate Reporting should look like (click to see our dynamic infographic), we also offered solutions. In 2015 we introduced a new approach to presenting corporate reports: Core & More.

Our Core & More concept presents corporate reports in a more connected and structured way; linking financial and non-financial information to accommodate diverse stakeholders’ needs. (See more in the links below.)

Since then, companies have gotten inspired to use Core & More in their annual reports. Two company representatives tell us about their experience:

Massimo Romano – Generali

Core & More fits in our aim for simpler, faster, and smarter corporate reporting: easier to manage, more effective in delivering and applying integrated thinking. It is really powerful to focus on the value creation story and the strategic information to connect the dots between reports, disclosing specific detailed information and break down siloes.

We have been able to leverage management commentary as our Core report and connect it to more detailed information in More reports. Applying Core & More came as a natural step in our corporate reporting evolution.

I think Accountancy Europe can help drive change by:

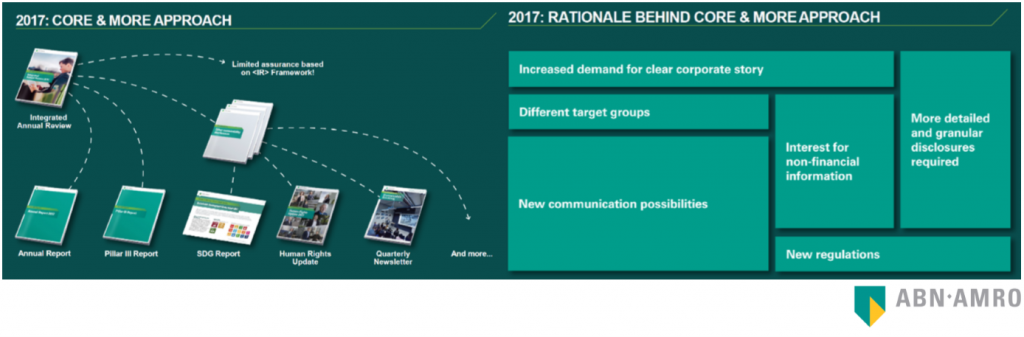

Tjeerd Krumpelman – ABN AMRO

We saw 3 things increasing: the number of regulatory requirements we had to comply with, the interest level in NFI, or pre-financial indicators as I like to call them from different stakeholder groups beyond investors, which then lead to our integrated annual report’s volume to rise to over 450 pages.

We needed a targeted approach to more concisely tell our story and address the interests from different stakeholder groups. We like Core & More because it gives the freedom to tell our true story: who we are and how we create value for stakeholders. It also allows to do so in a concise, clear and understandable way and in less than 100 pages.

Core & More enables us to really think about and decide what is our core message, what’s the story of our company and how we are performing, focusing on strategy and long-term value creation. That is why it worked so well to combine Core & More with the <IR> framework. We could not tell our story and focus on all mandatory aspects of reporting at the same time. We use the More reports to meet different stakeholder information needs without this very specific information cluttering the overview that reporting aims to provide. For example, regulators that mandate certain disclosures can find those in a specific More report.

I think Accountancy Europe can:

I believe that if Core gathers all essential corporate information relevant for all stakeholders, assurance should be sought on the whole Core report. For 2017 our Core got limited assurance based on the <IR> framework principles. This was new, our auditors had never done that before. Now we want to move towards more reasonable assurance on parts of the Core report, but we but feel there is some insecurity and reluctance towards this in the accountancy profession. NFI accountants enjoy this type of debate but their financial counterparts are less excited.