6 May 2021 — Publication

This document was developed with the advice of DG TAXUD, European Commission.

The changes to the EU e-commerce rules will take effect from 1 July 2021. This factsheet provides a high-level summary of the main changes and how accountants can support their SME clients. Time is of the essence.

The rule changes will greatly affect SMEs active in e-commerce. Accountants should research the changes as soon as possible to be able to inform and support their clients. We provide sources of additional guidance at the end of the document but further, specialist advice, may also be necessary.

Depending on their business model, the changes will have profound impacts on businesses. Since accountants are SMEs’ closest advisors, many small businesses rely on professional accountants to prepare for such rule changes, and for compliance with the rules. This is particularly important during the coronavirus crisis, with many SMEs’ attention focused solely on day-to-day survival.

To help SME clients through these changes, accountants should REACT:

From 1 July 2021 there will be two types of distance sales of goods:

From 1 July 2021, the VAT rules on cross-border business-to-consumer (B2C) e-commerce activities will change in the following ways for suppliers:

1. Change of Distance Selling Thresholds

A new EU-wide turnover threshold of EUR 10 000 will replace the existing thresholds for distance sales of goods within the EU. This will be a significant change for businesses making B2C intra-community distance sales of goods as Member States’ current thresholds are normally between EUR 35 000 and EUR 100 000.

Below this global EUR 10 000 threshold, the supplies of TBE (telecommunications, broadcasting and electronic) services and distance sales of goods within the EU may remain subject to VAT in the Member State where the supplier is established.

From 1 January 2025 other simplifications will become available to SMEs engaged in cross-border trade within the EU.

2. The Union One Stop Shop

The existing Union scheme of the Mini One Stop Shop (MOSS) is extended to cover both cross-border supplies of goods and services. A new online portal, the One Stop Shop (OSS), has been created. When their supplies of TBE services and intra-community distance sales exceed EUR 10 000, suppliers can declare and pay VAT due in all other Member States through the portal of their Member State of establishment. Otherwise, suppliers would have to register in each Member State where they make B2C distance sales.

The Union OSS will cover:

3. The VAT small item exemption will be removed

The VAT exemption for the import of small consignments of a value up to EUR 22 will be removed. This means all goods imported into the EU from third countries will now be subject to VAT, which would normally be collected from the customer by the national postal service or a courier service.

Collection of VAT from the customer can create issue in customer relationship due to delays caused by customs procedures and additional, often unexpected, charges. To avoid this issue, and to ease the process, the European Commission has introduced two optional systems:

4. Simplified Rules for Small Consignments – The Non-Union Import One Stop Shop

To simplify the declaration and payment of VAT for suppliers of goods that originate outside of the EU, a new special scheme has been created to cover distance sales of low value consignments goods imported from third territories or third countries, the Import One Stop Shop (IOSS).

This option can be chosen by suppliers when the value of the consignment does not exceed EUR 150.

Where the relevant criteria are met, online suppliers will have the option to register for the IOSS in one Member State. This Member State of registration will provide a single electronic portal to declare and pay the VAT on all distance sales of low value consignment goods throughout the entire EU. VAT will not be charged on the entry of goods into the EU and the suppliers can report and pay the VAT through a monthly return.

If the supplier is already established in a Member State, it must register for the IOSS in that Member State. If the supplier is not based in the EU, they will normally need to appoint an EU-established intermediary to fulfil their VAT obligations under the IOSS.

In order to benefit from the VAT exemption upon importation, a customs declaration is still required at the point of importation, which must state the IOSS VAT number (in the format of IMxxxyyyyyyz) that the supplier received on registration, so that it can be verified by customs services.

5. New Rules for Online Sales Platforms / Electronic Interfaces

Online platforms that are “deemed suppliers” will be responsible (jointly and severably with the actual supplier of the goods) for reporting and paying VAT on sales made by suppliers that use the platforms.

Platforms facilitating supplies of goods become “deemed suppliers” when they facilitate the distance sales of imported goods made by a seller and the goods are:

The OSS/IOSS online portals are also available to online platforms / electronic interfaces facilitating these distance sale of goods. Again, if the electronic interface is established outside the EU, they will normally need to appoint an EU-established intermediary to fulfil their VAT obligations under the IOSS.

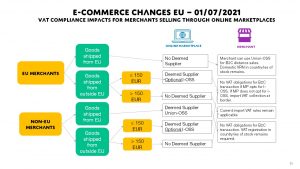

Suppliers can account for VAT on distance sales in the EU from 1 July 2021 by the routes indicated in the diagram below:

Accountany Europe factsheet Modernising VAT on recent changes to the EU VAT system

Explanatory notes on the new VAT e-commerce rules

Guide to the VAT One Stop Shop (OSS)

Factsheet for suppliers on the OSS

Factsheet for electronic interfaces on the OSS

Factsheet for suppliers on the Import One Stop Shop (IOSS)

Factsheet for electronic interfaces on the IOSS

Factsheet for businesses on the new VAT e-commerce rules

Explanatory notes for customs formalities for low value consignments

Contact details for EU Member States’ national OSS

2016 European Commission impact assessment on the VAT e-commerce rules

2017 package on VAT e-commerce: Council Directive (EU) 2017/2455

2017 package on VAT e-commerce: Council Regulation (EU) 2017/2454

2017 package on VAT e-commerce: Council Implementing Regulation (EU) 2017/2459

2019 implementing measures on VAT e-commerce: Council Directive (EU) 2019/1995

2019 implementing measures on VAT e-commerce: Council Implementing Regulation (EU) 2019/2026

2020 Commission Implementing Regulation (EU) 2020/194 laying down details on the working of the VAT OSS