8 July 2021 — Publication

Climate change, environmental degradation and social issues are global challenges that concern us all. Stakeholders understand that companies’ financial and sustainability reporting impact and depend on one-another. The demand for harmonised standards has pushed policymakers to take action.

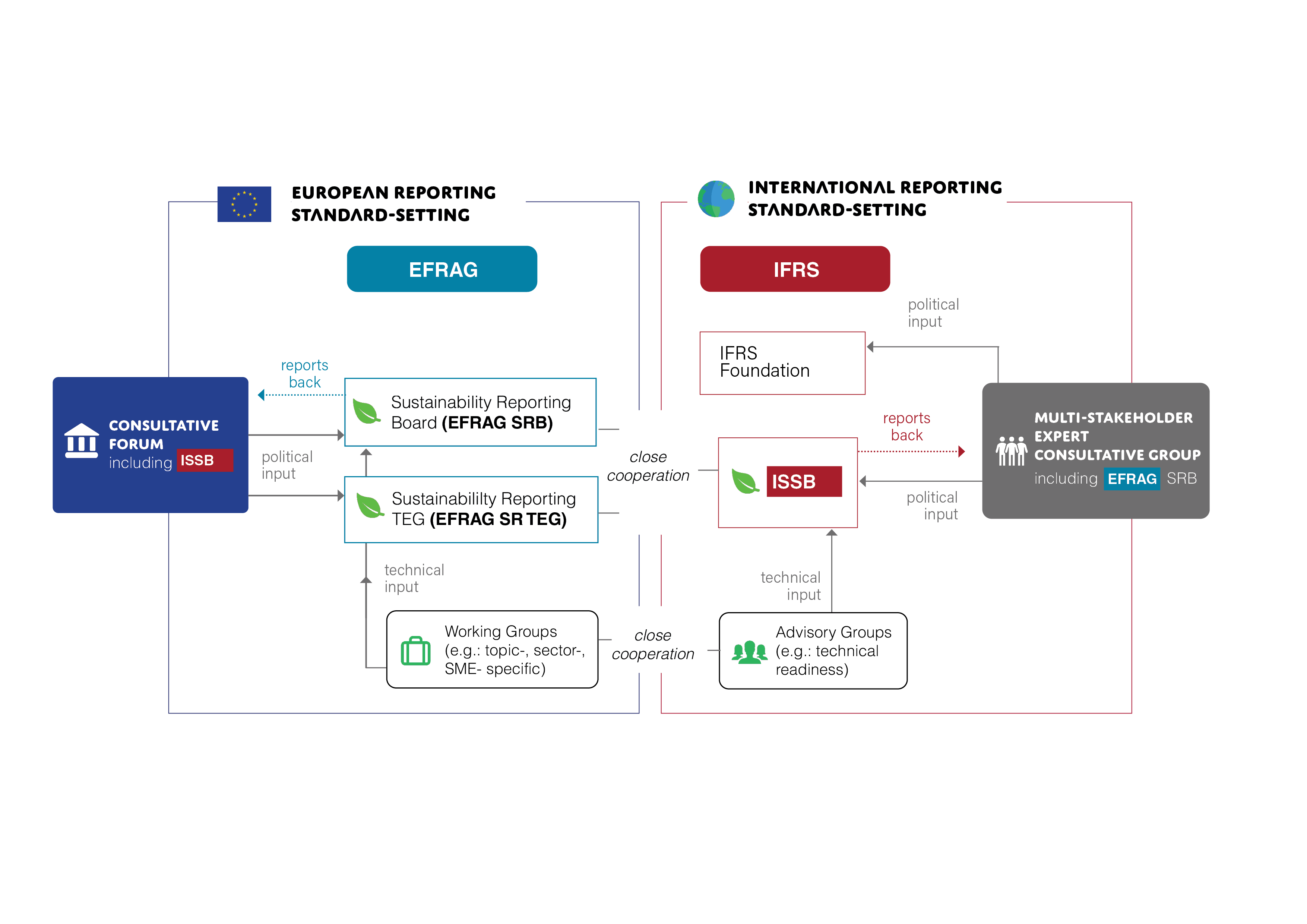

This publication presents the accountancy profession’s views on how to put into practice a constructive two-way cooperation to sustainability reporting standard-setting.

Indeed, the European Commission’s recent Corporate Sustainability Reporting Directive (CSRD) proposal requires all large and listed companies to apply EU sustainability reporting standards, which the European Financial Reporting Advisory Group (EFRAG) has been invited to develop. A sustainability reporting standards pillar is in the works at EFRAG along with a change in its governance structure. In parallel, the International Financial Reporting Standards (IFRS) Foundation is proposing changes to its Constitution to accommodate the creation of an International Sustainability Standards Board (ISSB).

We believe that cooperation between EFRAG and the IFRS Foundation is essential to produce aligned standards. Our paper lays down principles for cooperation and explores a collaboration on political and technical levels to secure consistency between reporting requirements. We will continue participating to this critical and strategic debate in the European public interest.