webinar

12 October 2020 (13:00 - 15:00)

Add to my calendarAvenue d'Auderghem 22-28, Brussels, Belgium

View on Google Maps

On 12 October, Accountancy Europe hosted a webinar on the implementation of the European Single Electronic Format (ESEF). The scope of the debate covered the opportunities, challenges and practical considerations about ESEF reporting and assurance. ESEF will be implemented from 2021, and there is an ongoing work by various stakeholders to be ready in time. Our webinar supported these efforts and contributes to an efficient and effective implementation. Watch everything that happened.

In his keynote speech, Alain Deckers (DG FISMA – European Commission) underscored that sustainability and digitisation are the two core elements of the European Commission’s (EC) agenda. Although the EU is leading globally on sustainability, on digitalisation, the EU is somewhat lagging.

“The message I want to convey is that we need to see ESEF as part of a broader strategy towards the digitisation of capital markets’ information available to capital market actors.”

– Alain Deckers

In these two areas, the EC has pursued several actions, such as, the revision of the Non-Financial Reporting Directive (NFRD). The responses to the relevant EC consultation demonstrated a strong demand for digital, preferably machine-readable, non-financial information. Another initiative, the CMU Action Plan, includes the establishment of a Single Access Point. This covers the accessibility of the information (both financial and non-financial as well as wider scope such as regulatory disclosures) and usability of the information (making it available in digital format).

If several Member States conclude that they would like to have an ESEF postponement, the Council will work together with the EC to make this happen. It remains to be seen whether this would be in the form of a legislative amendment or another mechanism.

The soon-to-be-released EC interpretive communication, will hopefully provide more clarity to the market on some practical aspects, including the audit of ESEF.

|

|

The European Securities Market Authority (ESMA) has the task of preparing and updating the ESEF Regulatory Technical Standards (RTS), which include the taxonomy and related requirements. ESMA’s website includes useful material, including an example of Annual Financial Report prepared in compliance with ESEF RTS. Anna Sciortino (Policy Officer – ESMA) encouraged stakeholders to review these along with the guidance available in IFRS foundation website.

“Even though … ESEF enforcement may be different in the EU Member States depending on how the Transparency Directive has been transposed, we are assured that in all Member States there will be a mechanism to enforce digital financial information.”

– Anna Sciortino

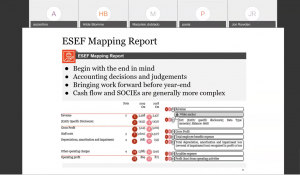

Issuers of ESEF should consider its preparation as a project and dedicate sufficient time and resources. There are many solutions offered by vendors and Jon Rowden (XBRL Leader – PwC United Kingdom) explained the essential factors that should be considered by issuers when making their decisions. He also emphasised the importance of preparing timetables and a mapping document.

“Begin with the end in mind. If you can take your financial statements and diagnose which tag is required for each and every disclosure, you have the answer. You know where you are trying to go!”

– Jon Rowden

|

|

The intended users will make decisions based on the digital information provided in this new format. Therefore, the data needs to be reliable. Reliability comes with assurance, and this is where the auditors come in. Marjolein Doblado (Chair, ISA Sub-group – CEAOB) described what is expected from the auditors with regards to ESEF. The CEAOB guidelines and the publication on ESEF Assurance prepared by Accountancy Europe and European Contact Group (ECG) are the main supporting documents available for auditors.

“The guidelines are intended to help further promote and facilitate consistency in various EU Member States. The auditor should obtain reasonable assurance about whether the financial statements are marked-up in compliance with ESEF requirements. The general approach to be taken regarding this compliance is well-known by auditors.”

– Marjolein Doblado

What will be the subject matter of these assurance engagements? Stefan Schmidt (Chair, ECG) clarified that there are two aspects that auditors will be looking at:

In addition, there will be a third aspect for Member States who follow the ‘two-document model’. Auditors in these jurisdictions will also check whether the digitally submitted financial statements are consistent with the audited financial statements.

“To perform an assurance engagement with due care requires the necessary resources and competence in the engagement team to be mobilised. This is probably one of the most important organisational aspects of an ESEF assurance engagement: to comply with ethical requirements!”

– Stefan Schmidt.

|

|

The panel started with the question ‘are we ready for ESEF?’

Moderator Hilde Blomme (Deputy CEO – Accountancy Europe) noted that there are still some uncertainties to be resolved at national level. Therefore, national competent authorities, national standard setters and public oversight bodies should clarify the procedures and issue guidance as necessary.

The panellists stated that preparations are ongoing, and the spread of the coronavirus had a significant impact since it is more difficult to engage in new projects for companies nowadays.

Then, the panel underlined the necessity and the benefits of consistency across the EU. Accordingly, if ESEF is to achieve its intended objectives, there is not much room for deviations in application.

Looking to the future, the panellists agreed that there will be more to come on digitalised corporate reporting, based on the needs and demands of users. ESEF should be considered as the first step into this new digitalised world. When the initial efforts are made and ESEF implementation is more mature, the for further digital corporate reporting will be easier to adopt.

“It has become clear that now is the time to start preparing for implementing ESEF, both for preparers and auditors. All beginnings are difficult but digitisation is the future so we should invest in it to be ready for that. This is really just the beginning.”

– Hilde Blomme

Watch here to see everything that happened (due to technical difficulties, the speaker order was slightly modified):

13:00 - 13:10

Hilde Blomme, Deputy CEO, Accountancy Europe

13:10 - 13:20

Alain Deckers, Head of Unit C1, DG FISMA

13:20 - 13:40

Anna Sciortino, Policy Officer, Corporate Finance and Reporting - ESMA

13:40 - 13:55

Marjolein Doblado, Chair, ISA Sub-group - CEAOB

13:55 - 14:15

Jon Rowden, XBRL Leader - PwC United Kingdom

14:15 - 14:30

Hilde Blomme, Deputy CEO, Accountancy Europe

Stefan Schmidt, Chair, European Contact Group (ECG)

14:30 - 14:55

Moderator: Hilde Blomme, Accountancy Europe

Panelists: Anna Sciortino, ESMA

Jon Rowden, PwC UK

Marjolein Doblado, CEAOB

Stefan Schmidt, ECG

14:55 - 15:00

Hilde Blomme, Accountancy Europe